Blockchain - What Is It?

Blockchain technology is surely one topic that is a little confusing to many people. Even I had trouble wrapping my head around it at first and wondered... how is this better? However, once you understand that it is closely related to spreadsheets and databases where information is entered and stored, it is a little easier. But, that is where the similarity ends, as the way the information is stored (in blocks), is entirely different - which brings incredible possibilities, elevated security, cost reductions, and extreme accuracy.

So, What Is Blockchain Exactly?

Blockchain is a revolutionary technology, developed back in 2008, that enables the creation of a tamper-proof digital ledger to securely record transactions shared to individual network nodes (different devices on a network). It employs a decentralized network, ensuring that no central authority governs the data. This unique approach safeguards transparency while ensuring security, making it an ideal solution for the digital age we have rapidly evolved into.

The blockchain technology functions through a series of interconnected blocks, with each block consisting of a distinctive code coined as a 'hash.' The purpose of the hash is to connect a particular block to the previous one, establishing a chain of information that is immune to any tampering or alteration. Such a decentralized and secure network makes it nearly impossible for any unauthorized party to modify or distort the data stored on the blockchain. The data blocks are then spread across multiple nodes (chain of blocks on multiple computers) in multiple locations and therefore, data cannot be manipulated at one node as the other blocks prevent any changes. This ensures that data entered is a permanent record.

How Does Blockchain Work?

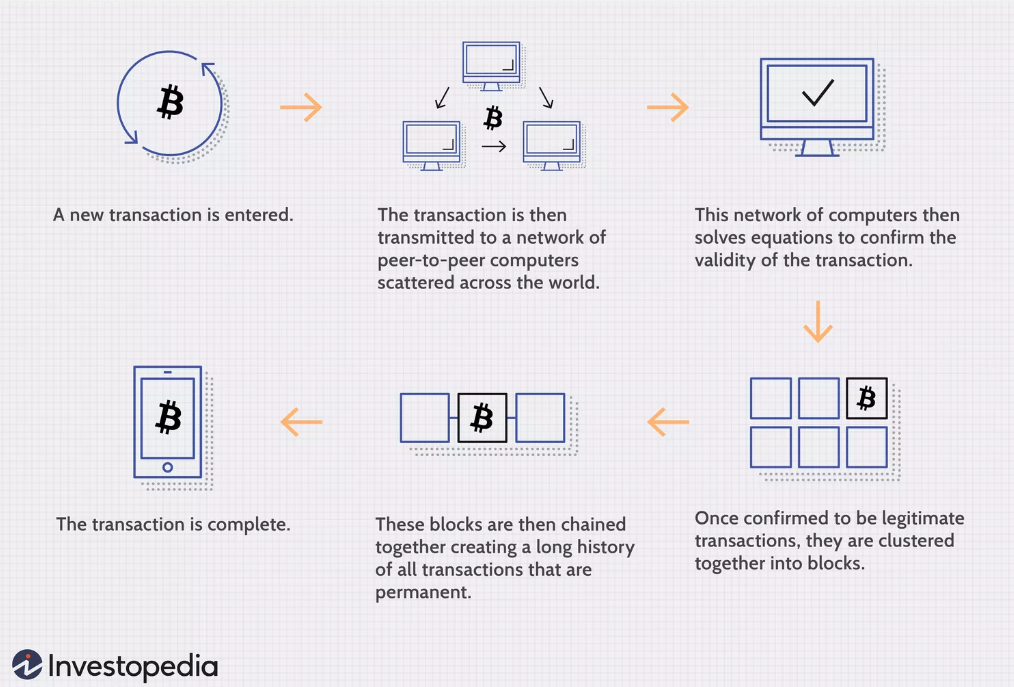

Now that you know what Blockchain is let's look at how it functions. Blockchain technology offers a highly secure and transparent means of carrying out transactions. The entire process involves a meticulous verification of transactions by multiple nodes before they are stored in a block. And as you can imagine, this requires a mass amount of computing power. Once the transactions are securely recorded in the blocks, the immutability (data entered is irreversible) of the blockchain technology ensures that they cannot be tampered with or deleted at any point in the future. This effectively eliminates the possibility of any fraudulent or malicious activity taking place within the system.

In order to ensure the utmost security of the blockchain, a complex series of algorithms are utilized to authenticate each and every individual transaction that occurs. The importance of this process cannot be understated, as it imposes a significant computational burden on any potential evil-doer who may seek to alter the data. Through the use of distinct hashing methods, the connection between each block in the chain is powerfully secured, resulting in an impressively strong and unyielding bond.

What Are the Benefits of Blockchain?

One of the main benefits of blockchain technology is increased security. Because each transaction is verified and encrypted, it is nearly impossible for someone to hack into the system and alter the data. This makes blockchain ideal for industries that require high levels of security, such as finance and healthcare. Privacy is also maintained as personal information is not publicly accessible in any transactional data.

Another benefit of blockchain is increased transparency. Because every transaction is recorded on a public ledger, it is easy to track and trace the movement of assets or information. This can help prevent fraud and increase accountability in industries like supply chain management, banking and finance. One great example, that we have all heard of, is Bitcoin. Bitcoin relies on Blockchain to securely record transactions between parties.

Due to having no central authority, several benefits now develop. Blockchain removes the need for 3rd party verification and therefore improves efficiency, lowers costs and improves accuracy, as humans and human errors are eliminated.

Problems With Blockchain

The issue of scalability presents a major obstacle for blockchain technology. As the number of transactions processed on the blockchain increases, so too does the overall size of the network causing expansions at an exponential rate which now raises the costs associated to expand processing power and network size. Under such conditions, it can be challenging for individual nodes to handle the processing demands in a timely manner, resulting in slower transaction times and higher fees. These factors could possibly hinder the broad adoption of blockchain technology.

A significant challenge facing the adoption of blockchain technology is the regulatory landscape. Due to the decentralized nature of blockchain, it operates outside the framework of traditional financial systems, making it difficult for regulators to keep a close eye on the industry. And, with different jurisdictions having varying rules and regulations surrounding blockchain, there is a lack of standardization, which can lead to uncertainty for businesses and investors alike. The ambiguity around compliance and licensing requirements can make it a daunting task to navigate the regulatory landscape, which can impede the growth of the blockchain sector.

Blockchain Use Cases

Blockchain technology has the potential to revolutionize a wide range of industries, from finance and healthcare to supply chain management. By providing a secure and transparent way to record transactions, blockchain can help businesses reduce costs, increase efficiency, and improve customer trust.

In finance, for example, blockchain is being used to streamline cross-border payments and reduce fraud. In healthcare, it is being used to securely store patient records and improve data sharing between providers. And in supply chain management, it is being used to track products from origin to destination, reducing the risk of counterfeiting, ensuring ethical sourcing practices and the ability to track source of contamination to related health issues.

At this stage, blockchain technology is considered to be in marginally more than a rudimentary phase. However, there is a considerable scope for progress in this field. One intriguing idea that is being explored is the possibility of amalgamating blockchain with the internet of things (IoT), which can produce incredible outcomes. This integration can provide secure and transparent communication between devices, enabling efficient and interconnected operations throughout the world. As of today, the IoT is quite insecure and frankly, a bit of a mess, but blockchain could very possibly turn all of that around.

Another promising avenue for further exploration is the implementation of blockchain technology in voting systems. This could mean deploying a decentralized and tamper-proof ledger to securely record every vote, potentially eradicating any possibility of fraudulent activities or manipulation This could make Trump very happy... or quite sad depending on how you look at it 🤣). If successfully executed, this would mark a definitive step forward in the way we conduct and manage elections, guaranteeing a fair and democratic process where each vote counts and contributes to the decision-making process.

Blockchain Adoption & Future

As of today, blockchain adoption is still in its early stages, with many industries exploring the potential of this technology. The finance industry has been one of the earliest adopters, with major banks and financial institutions investing heavily in blockchain-based solutions. In fact, a survey conducted by Deloitte found that 73% of financial services companies are either experimenting with or actively implementing blockchain technology. DeFi (Decentralized Finance) is expanding at a high rate of speed offering a far wider range of financial services, including lending, borrowing, derivatives, and insurance, as well as, offering people worldwide, greater control over their assets and investments.

Other industries, such as healthcare and supply chain management, are also starting to explore the benefits of blockchain. For example, blockchain can be used to securely store and share medical records, ensuring patient privacy and reducing the risk of errors. In the supply chain industry, blockchain can help to increase transparency and traceability, allowing consumers to track products from farm to table.

Blockchain is definitely evolving at a faster rate these days with developments in blockchain networks expanding through protocols from Polkadot and Cosmos, allowing data and assets to move across different blockchains with little effort. Aiding in blockchain's growth, are mechanisms like PoS (Proof of Stake), which is enhancing scalability, NFT's (Non-Fungible Tokens), are growing in immense popularity, which are units of data, on a blockchain, that represents a digital item, such as art, music, games or collectibles (we even see some of these pieces of art on our SMART TV's).

To Wrap It Up

In a nutshell, this cutting-edge blockchain technology possesses immense potential to transform industries by elevating their security, transparency, and efficiency standards to unprecedented levels. The potential use cases for blockchain are vast and impressive, ranging from supply chain management and healthcare records, to voting, finance, and even environmental and mining industry possibilities. Since my early IT days to now, it is evident that blockchain is no longer just a fleeting buzzword, but a current and tangible technology with immense transformative power that is poised to shape the world in meaningful ways for years to come.

Combine all of this with the explosion of AI and the possibilities of what can be achieved are going to be endless. And yes, Blockchain AI is in development. AI will be the brain analyzing the data and doing the decision making while blockchain will make AI more intelligent with the amount, and type of data it uses, while enhancing AI's infrastructure. The progression of this joint venture will need to be watched carefully. AI has its problems however, blockchain could greatly help with many of it's issues. It will be very interesting to see how it develops.

Hopefully, I have shed a bit more light and provided further understanding for you regarding what Blockchain is, how it functions, and where blockchain could take us. Let me know in the comments about your thoughts on blockchain, where you can see it's benefits or even where you could see further development possibilities.